Values are currently confined to a trading range of 74-80 with the possibility of a limited cease-fire developing into Ramadan which begins March 11th. The timing of OPEC meetings in March has yet to be set, which is surprising given how key these negotiations might be. Global stock levels have built during the first quarter despite the hostilities in the Middle East. The second quarter is certainly more questionable, with the potential for an increase highly dependent on OPEC deliberations and the continuation of voluntary cuts.

Natural Gas

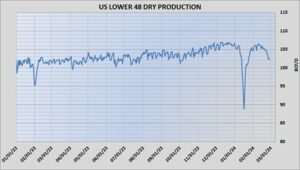

A steady drop in production levels has helped propel the market higher, with a 6.4 cent gain yesterday followed by an additional 7.7 cent improvement today as the April ended the session at 1.885. The slowing output, which has slipped toward 102 bcf/d, was the only positive fundamental. Weather remains tepid, with ample wind generation expected over the next two weeks to further dampen gas demand. Tomorrow’s storage report is expected to again be well below normal, with estimates in the 88 bcf area compared to the normal draw for this time of year at 143. To maintain the upside bias, production levels will need to at least maintain recent decreases and ideally continue to decline, which would heighten the potential for more substantial fund short covering than has been flushed out thus far. Today’s settlement exceeded the 20-day moving average, making the psychological 2 dollar level the next target, with the 38 percent retracement of the break since early January at 2.024. Any additonal fundamental negative, such as a smaller than expected stock draw tomorrow, could expose the fragility of the rally. There is no substantial support until the 1.75 area, and then the contract lows at 1.60.