by market analysts Stephen Platt and Mike McElroy

Price Overview

The petroleum complex fell sharply, with April crude losing 2.12 to settle at 76.49 as active selling developed in response to news that Israeli negotiators would take part in new Gaza ceasefire talks, which will take place this weekend in Paris with the US, Qatar, and Egypt. These will be the first negotiations on a ceasefire since Israeli Prime Minister Netanyahu rejected the last proposal by Hamas for a 4 ½ month truce. In addition, US sanctions announcement today did not appear to focus on Russian oil sales, but instead on financial institutions and the Mer system, along with entities providing military equipment and technology aiding Russia.

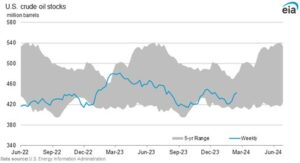

Yesterday’s DOE report showed crude inventories rising by 3.5 mb. In products, gasoline stocks fell less than expected by .3 mb while distillate lost more than expected at 4 mb. Total stocks of crude and products fell .8 mb. Domestic production was near record highs of 13.3 mb against 12.3 a year ago. Refinery utilization remained at 80.6 percent due to the Whiting refinery outage that is not expected to be rectified until early March. Total disappearance remains subdued at 18.9 mb compared to 20.2 last year. Gasoline disappearance was reported at 8.2 mb compared to 8.9 last year while distillate disappearance was indicated at 3.9 mb compared to 3.8 last year. Total net exports of crude and products reached 3.0 mb against 2.2 mb last year, with net exports 4.7 mb against at 3.9 mb in 2023.