Written Commentary

TODAY—INFORMA PRODUCTION—COMMITMENT OF TRADERS

Overnight trade has SRW Wheat down roughly 5 cents, HRW down 6; HRS Wheat down 2, Corn is down 3 cents; Soybeans down 7; Soymeal down $1.50, and Soyoil down 65 points.

For the week, SRW Wheat prices are up roughly 20 cents; HRW up 25; HRS up 2; Corn is up 14 cents; Soybeans up 14; Soymeal up $8.00, and; Soyoil down 105 points. Crushing margins are down 9 cents at $0.94; Oil share is down 1% at 31%.

Chinese Ag futures are closed for a week long holiday (Oct 1st thru 8th).

Malaysian palm oil prices were down 77 ringgit at 2,712 (basis December) at midsession tracking the drop in crude and soyoil prices.

U.S. Weather Forecast: The 6 to 10 day forecast for the Midwest has dry weather across all of the region through the period. Temps will be warming up to above average in the west and average in the east. The Southern Plains over the 6 to 10 day period has little to no rains for most of the region. Temps will be warming to average to above average early next week turning to above average for the rest of next week.

South America Weather Forecast: The Brazilian growing regions still has moderate rainfall for mostly Rio Grande do Sul over the next 10 day period with little rains elsewhere. By next weekend, light to moderate rains look to expand to areas north-central but still dry in the rest of the growing regions. The Argentine growing regions over the next 6 to 10 day period sees light rains to fall in most areas with some better precip amounts possible in the southern growing areas.

Europe/Black Sea Region Forecast: Not much change; plenty of rain seen in Western Europe over the near term. Eastern areas only receive light amounts of rain. Not much change; not much hope of drought relief in Russia’s Southern Region; any further relief in Ukraine is confined to the next three days favoring western portions of the nation; showers in the southern Balkan Countries will be welcome and temporarily beneficial to winter crop planting and establishment in the region, but brief delays to fieldwork will result through the weekend.

The player sheet had funds net sellers of 7,000 contracts of SRW Wheat; net bought 15,000 Corn; were net even in Soybeans; bought 5,000 Soymeal, and; net sold 6,000 Soyoil.

We estimate Managed Money net long 23,000 contracts of SRW Wheat; long 160,000 Corn; net long 217,000 Soybeans; net long 73,000 lots of Soymeal, and; long 93,000 Soyoil.

Preliminary Open Interest saw SRW Wheat futures up roughly 1,500 contracts; HRW Wheat down 825; Corn down 1,500; Soybeans down 950 contracts; Soymeal up 2,300 lots, and; Soyoil up 335.

Deliveries were ZERO Soymeal and ZERO Soyoil.

There were changes in registrations (Soymeal down 32)—Registrations total 109 contracts for SRW Wheat; ZERO Oats; Corn 361; Soybeans 1; Soyoil 1,907 lots; Soymeal 268; Rice ZER0; HRW Wheat 135, and; HRS 1,195.

Tender Activity—Syria seeks 50,000t optional-origin corn, 50,000t soymeal—Iran bought unknown quantities of optional-origin corn, soymeal—

For the week ended September 24th, U.S. All Wheat sales are running 8% ahead of a year ago, shipments up 4% with the USDA forecasting a 1% increase on the year

For the week ended September 24th, U.S. Corn sales are running 154% ahead of a year ago, shipments 71% ahead with the USDA forecasting a 32% increase

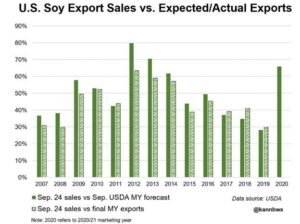

For the week ended September 24th, U.S. Soybean sales are running 169% ahead of a year ago, shipments up 64% with the USDA forecasting a 27% increase on the year

Wire story reports the new U.S. corn and soybean marketing year is just a month old, and the progress toward meeting big annual export targets is more advanced than normal in terms of sales, largely due to strong Chinese demand; U.S. corn and soybean export bookings stand at record levels for this early stage, and that bodes well for the expectation that 2020-21 shipments will rebound sharply from the dismal year-ago levels.

The USDA August soybean crush was pegged at 175 mil bu (estimate was 176 mil bu) versus 185 mil a month ago and 178 mil last year.

The USDA said 411 mil bu of corn was used for fuel alcohol in August, up from 424,000 mil a month ago and 455 mil last year.

Saskatchewan crop report: Conditions remained relatively dry throughout the province, allowing farmers to continue to make significant harvest progress; eighty-nine per cent of the crop has been combined, up from 77 per cent last week and well ahead of the five-year (2015-2019) average of 67 per cent for this time of year; an additional nine per cent of the crop is swathed or ready to straight-cut.

Brazil registers Sept exports:

—Soy exports were seen at 4.47 million tons versus 4.6 million tons in September 2019

—Corn exports in Sept came to 6.6 million tons, up from 6.44 million tons a year earlier

Argentina has temporarily cut soybean, soymeal and soyoil export taxes by 3 percentage points to 30% to help stimulate export revenue, the government announced, as the country struggles with recession and dwindling foreign reserves; the tax cut will last until the end of the year before being restored to 33% in January; we seek to strengthen the country’s international reserves; but farmers and analysts said the move might not be enough to significantly boost selling by growers and generate much-needed export dollars as the government heads into debt renegotiation talks with the International Monetary Fund.

Rising domestic prices for wheat, sunflower oil and sugar will lead to higher bread prices in Ukraine, Interfax Ukraine news reported, citing the Ukrainian bakers association; Ukraine is among the world’s major producers and exporters of wheat and sunoil and its exports largely exceed domestic consumption; the Ukrainian bakers association said the cost of wheat had jumped 40% this year, including a 25% rise in September

Euronext wheat edged lower on Thursday in step with Chicago, with farmer sales helping curb prices after a day-earlier jump triggered by lower than expected estimates of U.S. grain stocks; benchmark December milling wheat on Euronext settled down 0.75 euro, or 0.4%, at 197.00 euros ($231.36) a ton; it earlier ticked up to 198.50 euros, a new two-year peak for the contract and a fresh 4-1/2 month high for a spot price; Wednesday’s rally, which saw Euronext add nearly 3% while Chicago wheat climbed 5%, prompted selling by producers in Europe.

Asian demand for Australian wheat is expected to bounce back in the months ahead as the country is estimated to produce its biggest crop in four years, offering stiff competition to suppliers in the Black Sea region; around 1.5 million tons of wheat is scheduled to be shipped out of Australia in December with more than one million tons heading to Asian destinations led by China, the Philippines and Vietnam.

Malaysia is anticipating the United States to ban the imports of another plantation firm, after the U.S. Customs and Border Protection (CBP) agency blocked entry of palm oil products from FGV Holdings over forced labor allegations; another big firm will be banned soon, the Human Resources Minister said; he declined to name the company, but said it was a large firm within the plantation sector; industry analysts warned that the ban on FGV could lead to buyers in other countries turning away from the company or shunning Malaysian palm oil.