by market analysts Stephen Platt and Mike McElroy

Price Overview

Renewed liquidity concerns within the US banking system cut short a rally attempt that had carried values to the 70.00 area yesterday, with new lows reached today at 65.17. The early strength reflected the potential for a recovery in demand from China, possible Strategic Petroleum Reserve purchases, and ideas OPEC+ might act if the market looks to be moving toward imbalance. Concerns over the financial system undercut the rally attempt and led to large scale liquidation and stop loss selling as risk-off sentiment engulfed commodity and financial markets. The weakness, which has taken values down to levels not seen since December of 2021 reflects growing concerns of a recession, as tightness in credit markets potentially limits spending and derails recent signs of economic recovery. Fed policy is likely to be throttled back, the question of how much is certainly in the background following the bank bailouts to address concerns in the US and Europe.

Pressure on the Fed to raise rates has been ratcheted down as inflationary expectations weaken due to the banking problems. Next week’s meeting will be a key marker for the course of monetary policy, along with any additional problems that may emerge in the banking system.

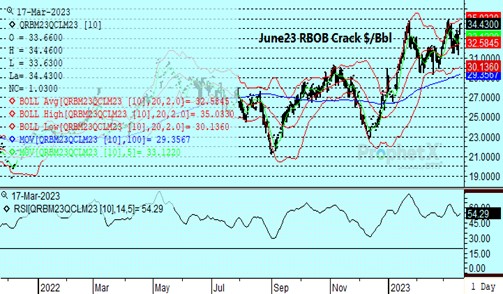

These economic concerns, along with recent expansion in refining capacity in Kuwait and at Exxon’s Baytown refinery, have had little impact on the crack margins, as the June RBOB crack has remained strong. A move through the 34.70 area could be a signal that the market is expecting a stronger economic trend into the summer months, contrary to current sentiment.