SOYBEANS

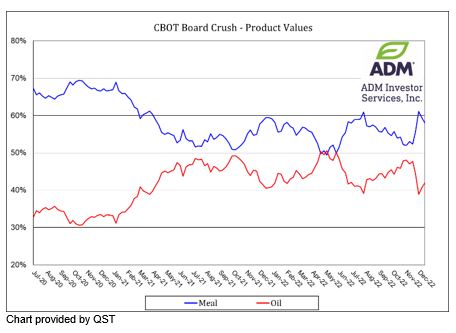

The soybean complex closed higher across the board. Jan-23 soybeans closed at $12.79 up $.11 ¼ for the day and down $.01 for the week. Prices remain in a $14.60 – $14.95 range. Jan-23 soybean meal closed at $455.30 up $3.30 for the day but down $7.70 for the week. Jan-23 soybean oil closed at 65.93 up .13 for the day and up 2.57 for the week. Spot board crush margins improved $.12 this week to $2.48 bu. Soybean oil product value jumped 1% to 42%. The USDA announced the sale of 124k tons (4.5 mil. bu.) of soybeans to an unknown buyer. Argentine soybean plantings advanced 10% last week to 61% complete, still well behind the historical average of 79%. Ratings slipped to 12% G/E, down from 19% last week. Parana, the 2nd largest producing state in Brazil is expected to harvest 21.4 mt of soybeans this year, up from YA drought reduced crop of 12.3 mt. Much needed rains of .50” – 1.00” are expected across Central Argentina the next few days. A dry but a cooler pattern to develop the last week of the year. Week 2 of the outlook offers better prospects for rains across Central Argentina the first week of 2023. The Week 2 forecast and beyond will be the principal factor driving prices next week. The markets do not reopen until 8:30 CST on Tuesday Dec. 27th. A much more favorable weather pattern with frequent showers and no threatening heat for Brazil, including the South, thru the first full week of the New Year. I suspect Brazilian production estimates will start trending higher. Argentine crop estimates will hinge on weather conditions in early January.